Large market disruptions and technological advances have gone hand-in-hand for as long as I can remember. We have seen massive changes in market fundamentals after the emergence of the Internet. In 2008, the implosion of the financial markets and OEMs, particularly in housing industry, occurred simultaneously with the emergence of APIs that dramatically changed the way systems could talk to each other. 2020 brought COVID shutdowns, a fundamental change to the way we work, 0% federal interest rates, and an explosion in the number and scale of the startup market.

Smart businesses find ways to leverage disruptions into new markets or advances while insulating themselves from the risks associated with those disruptions. There is a risk of engaging in new technology (see also all the failed blockchain startups) and waiting too long to adopt. I have a couple of business leaders I am talking to trying to figure out how to make use of the emergence of AI with all the confusion that goes along with not being deep in the tech weeds (sometime in the last 6 months we started to refer to ML algorithms as AI, which is fascinating).

The difference with AI now is both the speed of its emergence and how much it has had a direct-to-consumer launch without guardrails. So, let’s talk in plain English, or at least plain Jennie which is close enough, about what’s going on in this AI revolution and how to insulate yourself from risk while taking advantage of emerging opportunities.

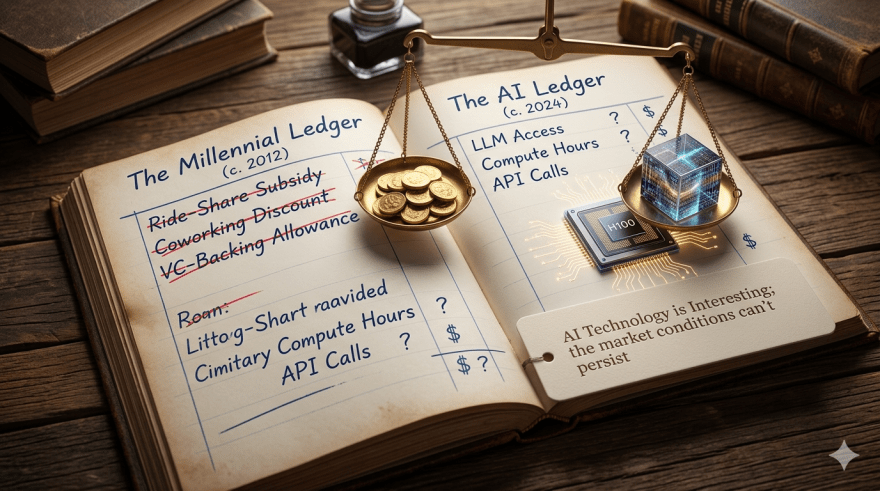

Millenium Lifestyle Subsidy

In two times in my working history, the Federal Reserve set interest rates to near-zero: Dec 2008-Dec 2015 during the Great Recession (remember “too big to fail” and poor Lehman Brothers) and March 2020-March 2022 during the COVID pandemic. I’m not here to debate the Federal Reserve or the macro economic impact of these moves. Instead, let’s talk about how this impacted business decision making, and is still impacting us with AI adoption.

Suddenly, for a lot of companies, money was essentially free. You are a VC sitting on access to capital and the cost of investing has plummeted, what do you do? You start investing in a wider portfolio of companies because your risk of choosing wrong, and losing your investment, has gone down. You are a person with an interesting idea of something to take to market and now you suddenly have a huge inflex of funding opportunities. Not only did this increase the number of startups in the market, it also fundamentally changed the metrics on which those startups were judged. Instead of looking for profitability as a major indicator of success, the metrics shifted to adoption. The goal was attaining customers, get them hooked on the freemium model, and show explosive growth. Instead of ARR (annual recurring revenue) we started tracking MAU (monthly active users). It’s not that the goal posts moved, the entire field shifted.

An interesting side effect of this was that the VC money drove down the price of these services, which were often below the cost to serve. Good examples are transportation gigs like Uber, meal prep kits like Hello Fresh, restaurant food delivery like DoorDash, and coworking like WeWork. There was an explosion of these services that were tech driven, VC backed, and low cost. Someone far more clever than I labeled this phenomenon the “Millennial Lifestyle Subsidy” (Derek Thompson, staff writer at the Atlantic was that person: original article in 2019 , follow up article in 2022). Then once capital got more expensive, VCs started to look for actual returns, the market matured, and inflation/labor costs increased the subsidy dried up and now these services are starting to cost market rate. Which results, naturally, in an exit of customers followed by an exit of providers.

AI’s Eating All the Capital

The same thing is happening in AI right now. The cost of data centers, high performance chips, and the very expensive engineers building AI right now is not reflected in the cost of commercially available AI. This time it’s not because of the low cost of money (as of this writing the Fed just maintained the fed funds rate at 3.5-3.75% with the effective funds rate holding steady at 3.64%… that is a far, far, far place from 0%- 0.25% the quantitative easing in March 2020). Ith’s because of massive circular financing arrangements between major AI labs, hardware providers, and cloud hyperscalers. Let me go a little deeper on that. The big companies that are building the data centers, the companies that build the chips that go into those data centers, and the AI tech companies that will use that compute are basically trading money between themselves to fund these deals (great visual of this). Which means there is no actual money being made here. Also, the majority of this technology has a 3 year lifespan, likely less because of Moore’s law, but it’s being depreciated over five to six years. Many folks have called out this puzzle, in particular The Economist has done a great job of laying it all out.

The commercially available tools will get more expensive. They must. It may take years before we fully see this play out. It may also come sooner with both OpenAI (ChatGPT) and Anthropic (Claude) planning on going public this year. But we are already starting to see cracks in OpenAI’s dominance as competition heats up and the return on investment stutters. Disney pulled out of a licensing deal where the ink was still wet, Walmart shelved their agentic checkout integration after returns didn’t live up to hype, Microsoft restructured their deal to move into a more competitive framing, Nvida’s $100B investment has stalled, and there is the start of user boycots after signing a deal with the US military. All of this breaking news has happened to OpenAI in the last month. However, this isn’t just one company starting to fray, I believe this is early signs of the high investment and low returns of these models starting to wear thin. There will not be one winner take all in this market, it will be a fragmented offering which will result in a lower market cap/multipliers for all the companies involved.

Real World, Real Applications, Normal People

Okay, Jennie, that’s all interesting and a bit scary about the long-term state of our economy. And we haven’t even talked about the geopolitical risks of China’s heavy investments, and the vulnerability of the Taiwan based chip development industry. But what do I, average person, do with all this?

Great question! Here’s the good news. Much like the millennial lifestyle subsidy, this all means that the AI technology we are seeing right now is artificially inexpensive. While it is cheap to experiment, you should experiment using the commercially available tools. There are tons of articles out there about when you should use Gemini vs ChatGPT vs Claude vs CoPilot. There are also tons of resources out there for when you should tap industry specific instead of generic models. It is worth spending some time seeing what these tools can do and what use cases they can easily automate. But… use caution.

If you have integrated an AI tool into a core business process and then forget how to do it without the AI, you will be in trouble when the price starts skyrocketing. As with any vendor relationship, you should do your due diligence to understand what kinds of agreements and protections you have from the technology. If you are building with AI embedded in your software, what kinds of integration layers do you have in place to easily switch vendors or processes to a more traditional automation process if you need to? At what point in understanding how the tool works, and clearly building the business case for the efficiencies gained, does it make sense to look at owning the means of production instead of relying on a vendor? E.g. when do you roll your own LLM or voice agent? All of these set points and risks will be different for different businesses.

I think it is also super important to think about what AI will convince you that it’s good at but it’s not. AI doesn’t make decisions. And AI doesn’t create, it plagiarizes (notably recently the novel Shy Girl was pulled because it was written by AI which was a contractual violation). Also, I have customers (in B2B environments) starting to push back on vendors that they don’t want their data to be used by AI.

The technology is interesting; the market conditions can’t persist.

I had started this article planning on talking about a bunch of trends I am seeing in the market with AI. But I so love the millennial lifestyle subsidy aspects of the market conditions right now I got overly verbose. In simpler words, Jennie geeked out too much. So, we are gonna call this part one and come back soon with part two.

Note: I don’t use AI to help write my posts or create example pictures. I do use AI to create the header image. In this case I prompted Claude (Anthropic), Gemini (Google), ChatGPT (OpenAI) and CoPilot (Microsoft/GitHub) by giving it my blog post. CoPilot hit its limits for creating images because my husband used all our free tokens making complex spreadsheets for fun. I had to give all three multiple chances to create a good header image. The initial passes were really bad. Gemini won. I also asked them all to give me a title and LinkedIn summary. ChatGPT made me realize my thesis should be my title (my working title was Business Models Meet AI: Millenium Lifestyle Subsidy). Claude did the best job of asking the right questions and generating a starting LinkedIn summary I iterated on. Still too many em-dashes (:fist-shaking:).